Make Your Next Trip Extraordinary

Overseas Credit Card Purchases: Which Currency Should I Pay With?

Keeping track of currency exchange rates is a necessity when traveling. Thankfully, there are many apps for that task, so we don’t have to spend too much of our time doing the research (I like Easy Currency Converter; leave your favorite in the comments below). But while it’s helpful to know the rough exchange for your home currency, the actual conversion rate varies from bank to bank, credit card to credit card, and even local merchant to local merchant.

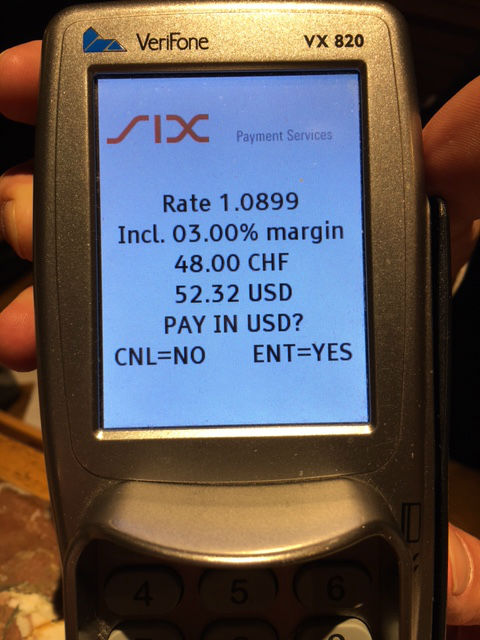

As a result, when you’re overseas and you use a credit card, you’ll often see that the payment machine asks whether you want to pay with U.S. dollars or the local currency. Which one should you choose, and why?

Overseas credit card machines offer currency options. Which should you choose? Photo: Lindsay Lambert Day

First: Use the right credit card.

Having a credit card that’s ideal for travelers is your first line of defense against currency pitfalls: The good ones waive all foreign-purchase fees. “When you make purchases abroad, you should be using a card that doesn’t add foreign transaction fees to your bill (which can be as much as 3%),” says credit card expert Gary Leff, of View From the Wing. “All cards are going to convert foreign currency to your home currency, and you’ll get the prevailing rate. Some cards, though, will charge you a fee on top of the conversion rate to do it.”

Second: Pay in local currency.

“When a merchant outside the U.S. asks whether you want to be charged in U.S. dollars or your local currency, always say local currency,” advises Gary. “That’s because [the merchant is] going to hit you with their own conversion rate (likely unfavorable, but certainly not as good as the one you will get from your card company). And then, if your credit card hits you with foreign transaction fees, they’re going to charge those fees anyway, even if you paid in U.S. dollars, because it’s a foreign-made transaction.”

The final word:

“There is almost never any benefit to being charged by a merchant in your home currency,” Gary says. “You are best off having your credit-card-issuing bank do it at their rate. And you want to make sure you’re paying with a card that doesn’t charge you for the privilege of making purchases abroad.”

Be a smarter traveler: Read real travelers’s reviews of Wendy’s WOW List and use it to plan your next trip. You can also follow her on Facebook, Twitter @wendyperrin, and Instagram @wendyperrin, and sign up for her weekly newsletter to stay in the know.

7 Comments

Post a Comment

Stay in the Know With Our Newsletter

I think they’re trying to take advantage of tourists inexperienced in foreign travel who like the comfort of knowing the price in their home currency. (Du-uh!) Anyway, usually the merchant’s bank charges 3–4%, so it’s almost a wash for customers whose cards have a 3% foreign CURRENCY fee. But for those unlucky cardmembers who are subject to a foreign TRANSACTION fee, it’s a double-whammy!

But ATMs (UK term: cashpoints) in Canada wanted to charge me a 7% fee when using my debit card to withdraw (vs. within a quarter % of mid-market by my bank at home!)

No, if you choose local currency, the credit card company (Visa, etc. — not the merchant’s bank) will convert the charge, and they will use the “prevailing rate”, which is typically about 1% worse than the interbank rate you’ll see online. When the merchant offers to convert it, it’s usually about 3% worse than that.

There are many situations that the merchants do not offer a choice of currency and default to your home currency seeing that it’s a foreign credit card. Also even if you checked the local currency box, the merchants may not apply that selection and you end up paying the extra four percent when you receive the statement.

If you ask to pay local currency and they convert to dollars at a bad rate, I’d protest the transaction as fraudulent. Also, if a merchant like Hertz quotes a local price and then insists on converting to dollars, I’d refuse to pay. Of course, if they quote the price in dollars, that’s their right.

Hertz Heathrow refused my request to charge in Pounds on car return. I was told corporate policy is to charge in the currency of the card issuing country, at Hertz conversion rate. Not negotiable.

Avoiding dynamic currency conversion is tough, but important. It can also happen with ATM withdrawals, not just credit cards. ALWAYS charge/withdraw in LOCAL currency.

Most major tour operators in Mexico will only accept USD for payment…I made the mistake of charging these to my Hotel bill for the extra hotel points, and of course they converted it back to pesos at an unfavorable rate.